Is AssetMark Good for 401k? Review, Fees, Pros & Cons

AssetMark is a retirement services provider that offers 401(k)

- Plan solutions

- Investment management services, and

- Advisory support for employer-sponsored retirement plans.

Investors evaluating an AssetMark 401(k) typically look at how the plan compares with other available retirement options and whether it meets their long-term savings needs.

AssetMark, Inc. is a fee-based investment adviser and wealth management platform headquartered in Concord, California.

It operates as a turnkey asset management platform (TAMP), helping advisors deliver professionally managed investment solutions while improving operational efficiency.

- Managed investment portfolios

- Asset allocation and portfolio construction solutions

- Advisor technology platforms

- Practice-growth consulting

- Investment research and operational support

AssetMark is one of the leading wealth management platforms serving independent financial advisors in the United States. With over $160 billion in platform assets, a nationwide advisor network, and backing from GTCR, the company continues to expand its role as a technology-enabled partner for the independent advisory industry.

What is AssetMark and How does it work?

AssetMark is an independent wealth management technology firm serving financial advisors, providing digital account access, investment management, and back-office support.

AssetMark Retirement Services handles 401(k)/403(b) plan services.

Plan sponsors can elect bundled service or unbundled service.

AssetMark itself does not hold the plan assets. Instead, plan accounts are held at third-party trust custodians.

How AssetMark Manages 401(k) Plans

Employer Engagement

AssetMark works through financial advisors to help employers establish retirement plans. It evaluates the company’s goals, workforce profile, and desired level of support before designing a solution.

Choose the Service Structure

AssetMark provides different levels of support depending on the employer’s needs:

- Bundled: investment management with recordkeeping and administrative support.

- Unbundled: AssetMark manages investments, outside providers handle admin.

- 3(38) fiduciary: AssetMark selects and monitors the investment lineup.

- PEP: fiduciary investment oversight, admin handled by partners.

Build the Plan

AssetMark helps customize key plan features, including eligibility, employer contributions, vesting, safe harbor design, and investment options, based on the employer’s objectives and employee demographics.

Launch and Connect Systems

Once the plan is approved, AssetMark helps establish the operational framework, including participant setup, payroll integration, contribution processing, and coordination with third-party administrators when required.

Manage Investments and Fiduciary Oversight

Depending on the arrangement, AssetMark may provide investment advice or discretionary 3(38) fiduciary management. This includes monitoring investment options, conducting due diligence, and maintaining the plan’s investment strategy.

Support Participants and Sponsors

Employees access their accounts through digital tools to review balances, manage contributions, and make investment elections. Employers and advisors receive reporting and ongoing support to monitor plan performance.

AssetMark provides a flexible 401(k) framework that combines investment management, fiduciary support, and retirement technology to help advisors and employers deliver effective workplace retirement solutions.

Its role can scale from investment oversight to broader plan support, allowing sponsors to choose the level of involvement that fits their needs.

Thinking About a Solo 401(k)?

AssetMark 401(k) Investment Options and Features

AssetMark’s retirement platform delivers institutional-quality investment lineups curated by its in-house due diligence team.

Professionally Managed Investment Lineup

- Curated retirement investment options giving smaller plans access to institutional-style solutions.

- Investments are selected and monitored through AssetMark’s due diligence process.

Model Portfolios

- Professionally managed portfolios based on risk levels, retirement goals, and target retirement dates.

- Regularly reviewed and rebalanced, with 3(38) models allowing AssetMark to manage investment selection and oversight.

Mutual Funds and ETFs

- Diversified options including equity, fixed-income, international, and specialty strategies.

- AssetMark’s team monitors investments for performance, cost, and risk, making changes when needed.

Specialized Investment Choices

- Additional portfolio options including ESG-focused, faith-based, and custom investment mixes.

- Allows plans to better align with participant values and goals.

Index and Active Investment Options

- Low-cost index funds for broad market exposure.

- Actively managed funds where additional expertise is desired.

- Lineup can be structured around the plan’s objectives and participant needs.

Self-Directed Brokerage Account (SDBA)

- In-plan brokerage option for eligible participants to access a broader range of investments.

- Remains within the retirement plan ecosystem.

Digital Tools and Retirement Resources

- Online tools supporting retirement planning, account visibility, goal tracking, and investment management.

- AssetMark’s advisor tools help with planning scenarios and portfolio oversight.

AssetMark aims to deliver large-plan capabilities such as:

- Diverse menu

- Professional management

- QDIA selection

- 404(c) compliance for smaller-plan clients.

AssetMark Fees

AssetMark’s fee structure for retirement plans is primarily asset-based, consisting of

- Platform fee to AssetMark Retirement Services and

- Advisory fee charged by the financial advisor overseeing the plan.

These are typically combined and paid from plan assets on a quarterly basis.

| Cost Component | Typical Cost | Who Receives It | What It Covers |

|---|---|---|---|

| AssetMark Platform Fee | ~0.20%–0.30%+ | AssetMark | Platform access, administration, custodial services, and brokerage support. |

| Advisor Fee | ~0.30%–0.50% | Financial Advisor | Fiduciary guidance, investment oversight, retirement planning, and participant support. |

| Investment Expenses | ~0.10%–0.80% | Fund Providers | Ongoing mutual fund or ETF operating expenses and portfolio management costs. |

| Recordkeeping / Admin | Often bundled | Provider / TPA | Participant recordkeeping, compliance testing, reporting, and plan administration. |

| Setup / Conversion | $500–$5,000 (if charged) | Provider / TPA | Initial plan setup, onboarding, conversion, and implementation services. |

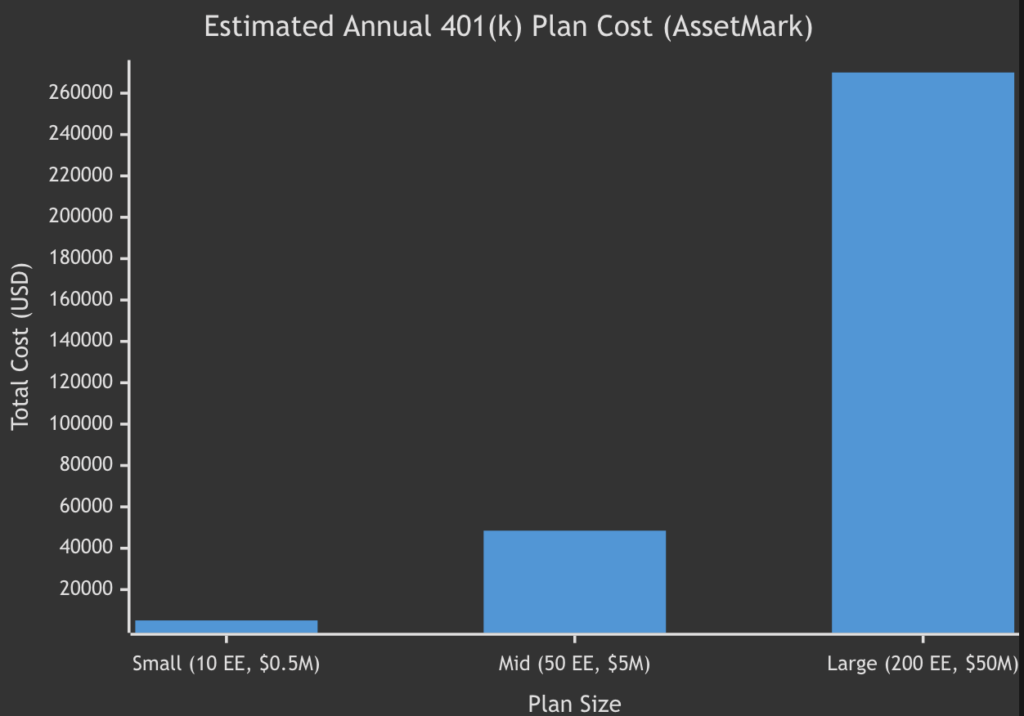

Because many retirement-plan fees are asset-based, the total cost impact varies significantly by plan size.

The examples below demonstrate how advisory, platform, investment, and administrative costs may combine in practice.

| Plan Size | Assets | Estimated Total Cost | Approx. Cost % |

|---|---|---|---|

| Small | $500K | ~$5K–$8K/year | ~1.0%–1.5% |

| Mid | $5M | ~$50K–$65K/year | ~1.0%–1.3% |

| Large | $50M | ~$500K/year | ~1.0% or lower |

AssetMark provides fee schedules and required disclosures, but employers and plan sponsors should request a plan-specific proposal to understand the total expected costs for their retirement plan.

Pros and Cons of Using AssetMark for a 401(k)

Pros

- Built-In Fiduciary Investment Support

- Institutional-Style Investment Options

- Dedicated Advisor and Plan Support

- Flexible Service Model

- Supports Multiple Retirement Plan Types

- Technology and Digital Tools

Cons

- Higher Total Cost

- Requires an Advisor Relationship

- Limited One-on-One Participant Advice

- Regulatory History

- Custody and Fee Transparency Review Needed

AssetMark is a strong option for employers seeking a professionally managed retirement plan with comprehensive advisor support and flexible service options.

But its value proposition is strongest for sponsors who prioritize fiduciary oversight, service, and investment expertise over minimizing costs.

Who is AssetMark Best Suited For?

AssetMark is best suited for small to medium-sized employer plans (roughly $1–50 million in assets) that want advisor-led service.

- Independent RIAs looking to expand into retirement planning for small businesses.

- Businesses with limited in-house HR resources.

- Plans whose owners or employees desire professional investment management.

- Faith-Based and ESG-Minded Firms: AssetMark’s specialty portfolios can attract churches, schools, or companies that want specific screens in their plan lineup.

- AssetMark can serve very small plans, even a solo 401(k), up to mid-sized enterprises.

Comparisons to Other Providers

Below is a high-level comparison of AssetMark with other common 401(k) providers:

| Provider | Services | Fee Structure | Best For |

|---|---|---|---|

| AssetMark | 3(38) fiduciary, model portfolios, flexible bundling, advisor support. | Asset-based fee (advisor + platform) + fund expenses. | Small–mid plans with dedicated advisors. |

| Fidelity | Full-service recordkeeping, fiduciary options, participant education. | Participant fees + fund expenses; pricing varies. | Small to large employers seeking low-cost solutions. |

| Vanguard | Low-cost index investing, recordkeeping through Ascensus. | Per-participant fee + low asset-based fee. | Small–mid plans focused on low investment costs. |

| ADP | Payroll-integrated recordkeeping and administration. | Base fee + participant fees + optional AUM fee. | Small businesses using ADP payroll. |

| Charles Schwab | Recordkeeping, brokerage window, fiduciary options. | Custom pricing with participant and asset-based fees. | Small–mid plans with Schwab relationships. |

Notes: Fee structures vary by plan size, investment lineup, and negotiated pricing. Investment expense ratios are typically separate from provider administrative fees.

Actual pricing should be confirmed through a provider proposal.

Questions to Ask Before Choosing AssetMark

Asking these questions upfront can help you understand the full scope of AssetMark’s services and compare costs accurately.

It can help determine whether the platform aligns with your organization’s fiduciary responsibilities, budget, and retirement plan objectives.

AssetMark Retirement Services FAQs

AssetMark Retirement Services is a division of AssetMark that provides retirement plan administration and investment management for employer-sponsored plans.

Client assets are held by independent custodians. AssetMark manages the plans but does not custody client funds.

No. AssetMark manages the plan’s investment lineup but does not provide personalized investment advice to participants.

AssetMark supports a wide range of retirement plans, including 401(k), 403(b), SEP, SIMPLE, Solo 401(k), and defined benefit plans.

Yes. AssetMark integrates with many third-party administrators and payroll providers.

Participants can access their accounts through an online portal and receive statements from the plan’s custodian.

No fixed minimum applies. AssetMark supports plans ranging from solo 401(k)s to large employer retirement plans.

In 2023, the SEC settled charges with AssetMark over disclosure issues related to certain fees. The company agreed to improve its disclosure practices.

AssetMark coordinates the plan conversion and asset transfer with your advisor, custodian, and plan providers.

Possibly. AssetMark or its advisors may provide references or case studies upon request.

References: