Find My 401k With Social Security Number: 6 Databases to Search

Lost 401(k) accounts are more common than many realize, particularly after multiple job changes and incomplete rollovers between employers.

These retirement balances often remain tied to former companies or plan administrators, making them difficult to trace through standard records alone.

While several government and private tools allow searches using an SSN, there is no single database that provides a complete view of all retirement assets in one place.

Locating an old 401(k) typically involves working through

- Employer records

- Plan custodians, and

- Official search platforms.

| Resource | SSN Search? | What It Covers | Link |

|---|---|---|---|

| Department of Labor Retirement Savings Lost & Found | Yes | Employer retirement plans linked to your identity | https://lostandfound.dol.gov |

| National Registry of Unclaimed Retirement Benefits | Yes | Unclaimed 401(k) and retirement balances reported by employers | https://www.unclaimedretirementbenefits.com |

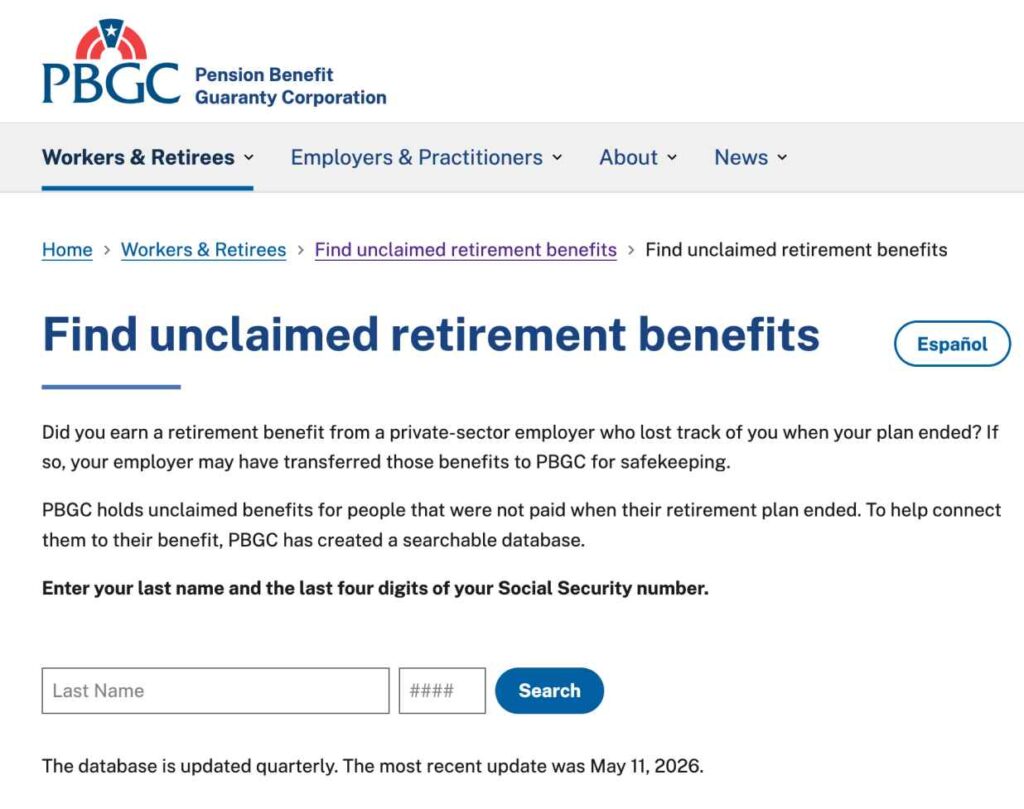

| Pension Benefit Guaranty Corporation (PBGC) | Last 4 digits | Pension-related unclaimed benefits from terminated plans | https://www.pbgc.gov |

| State Unclaimed Property Databases (NAUPA) | Often | Abandoned retirement checks and escheated funds | https://unclaimed.org |

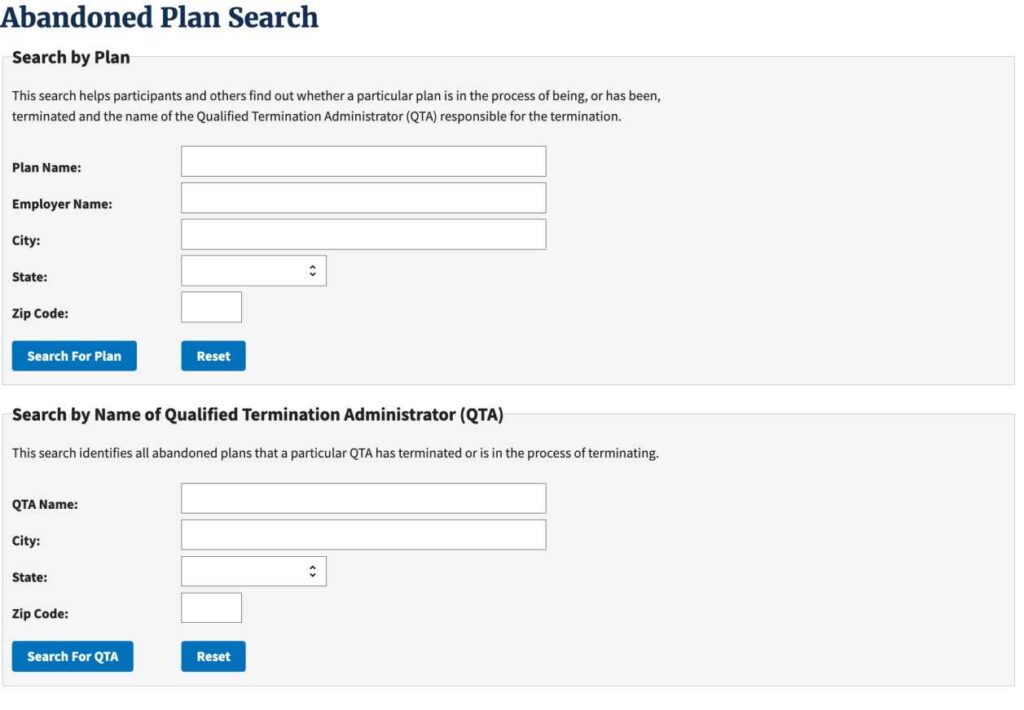

| DOL Abandoned Plan Search | No | Closed or terminated retirement plans | https://www.efast.dol.gov |

| Form 5500 Search (DOL eFAST) | No | Plan sponsor and administrator filing records | https://www.efast.dol.gov |

Can You Really Find a 401(k) With Your SSN?

Yes, but only indirectly.

Some official and private databases let you search using your Social Security Number or the last four digits of it.

Department of Labor’s Retirement Savings Lost and Found Database was created under SECURE 2.0 designed to help people locate retirement plans connected to their identity.

Database to Check Your 401(k)

A lost 401(k) can end up in several places. So, you need to search in several database.

Common places to check include:

1. Your former employer

The company that sponsored the 401(k), even if you no longer work there might still have your information.

Contact its HR or benefits department to get the plan name and administrator.

2. Plan administrator or recordkeeper

Firms like Fidelity, Vanguard, Empower, Prudential, or others may still hold the account.

If you remember or find on old statements which firm ran your 401(k), contact them directly with your name, and former employer to see if an account exists.

Plan-member portals or 401(k) websites often allow “forgot password” flows so you can regain access by verifying your info.

3. An automatic rollover IRA

Small balances are sometimes moved into an IRA if the plan no longer has contact with you.

Many plans automatically convert small balances often <$5,000 of separated participants into an IRA with the recordkeeper or in a collective trust.

For example, Fidelity and some others will auto-roll small accounts.

4. State unclaimed property

Uncashed checks or abandoned balances may have been sent to the state treasury.

If you left a job and were entitled to a distribution, the plan may have issued a check to your last known address.

If you never cashed it, the money could be sitting as unclaimed property or still with the plan administrator.

5. A rolled-over IRA

If you rolled an old 401(k) into an IRA or your employer did a rollover, it might live in that IRA.

Check any IRAs traditional or Roth, you have for incoming rollovers or larger-than-expected balances.

Look at old brokerage or bank accounts around your job-change dates.

6. Abandoned plan records

If the employer shut down or terminated the plan, special federal resources may still show where the money went.

Step-By-Step Process to Locate a Lost 401(k)

Before you start calling companies, it helps to organize the search.

1. Gather your records

Make a list of every job where you contributed to a 401(k). Then collect anything that may help identify the plan, such as:

- old W-2s,

- pay stubs,

- tax returns,

- 1099-R forms,

- old account statements,

- employer names,

- and your dates of employment.

This makes it easier to verify your identity and match the right account.

2. Use the Department of Labor’s Lost & Found Database

Create a Login.gov account and use it to access the Department of Labor’s Retirement Savings Lost and Found site.

After verifying your identity, enter your SSN to see whether any linked retirement plans appear.

This is usually one of the best first steps because it is official and free.

3. Search the National Registry of Unclaimed Retirement Benefits

This registry is another useful free tool.

It lets you search for unclaimed retirement accounts that employers or plan administrators have reported.

4. Check state unclaimed property databases

Search the state treasury or unclaimed property database in every state where you lived or worked.

If a 401(k) check was never cashed, it may have been turned over to the state.

5. Search PBGC records

For pension plan or terminated retirement benefit, the Pension Benefit Guaranty Corporation may have records that help you locate it.

6. Use abandoned plan tools

In case your old employer closed, merged, or terminated the plan, check the Department of Labor’s abandoned plan.

7. Look up Form 5500 filings

Old Form 5500 filings often list the plan administrator, trustee, or recordkeeper.

These can lead you to the right contact.

8. Contact the employer or administrator directly

Once you have a lead, call or email HR, benefits, or the plan provider.

Give them your name, dates of employment, and the last four digits of your SSN if needed.

9. Escalate if there is no response

If the employer does not respond, follow up in writing. Even contact the Department of Labor’s Benefits Advisor for help locating the plan.

A methodical approach usually works better.

A simple outreach template

When contacting a former employer or plan administrator, use this as template for your outreach:

You can say something like:

If they ask for more details, you can provide your former employee ID, dates of employment, and the last four digits of your SSN.

No single database finds everything, which is why using several tools gives you a better chance of success.

What to Do if the Company Went Out of Business?

If your old employer shut down, merged, or filed bankruptcy, the search can take a little more work.

Start with the abandoned plan search tool. If the plan was officially terminated, it may list the Qualified Termination Administrator, or QTA, who handled the final account records.

You should also check Form 5500 filings for the employer. Those filings may still show the final trustee, administrator, or distributor.

If the plan was a pension, PBGC records may help. If the business was acquired, the successor company may have inherited the benefits department or records.

Find My 401(k) FAQs

No. Official tools like DOL Lost & Found and PBGC searches require the account holder’s own identity verification. For deceased individuals, heirs must contact the plan administrator or employer directly with legal documentation.

Yes, if using official government sites such as DOL or PBGC. They use secure encryption and identity verification via login.gov. Always verify the URL before entering personal data.

No. The database is incomplete and still being populated. Absence of results does not confirm absence of an account. Other sources, including employers and state databases, should be checked.

Not by locating it. Taxes apply only upon distribution. Withdrawals are taxed as income, and may incur a 10% penalty if under age 59½. Rollovers to another retirement account are not taxable.

Yes, for official verification processes. At minimum, full identity details are required by plan administrators and government databases. Only share SSN information with verified institutions.

Yes, but it is usually unnecessary. Free government databases and employer contact methods are available. Paid search services may charge high fees and should be evaluated carefully.

Use both current and former names when searching or contacting administrators. Identity verification may require documentation such as a marriage certificate or legal name change records.

Only the U.S. SSN applies to U.S. 401(k) records. Foreign identifiers are not used in U.S. retirement plan databases.

Old plans may still exist under successor custodians or in the DOL Abandoned Plan Program. Some balances may also have been transferred to IRAs or state unclaimed property systems.

Typically 1–6 weeks for rollovers or distributions. State-held funds may take longer, often several weeks to a few months depending on processing time.

References: