Should I Pay Off My 401k Loan Early? Compare Scenarios & Alternatives

POINTS

-

Paying off a 401(k) loan early reduces the risk of taxes and penalties if you leave your job.

-

Early repayment lets more of your retirement savings stay invested.

-

Pay off high-interest debt before accelerating a low-interest 401(k) loan.

-

Keep your emergency fund intact before paying off your 401(k) loan early.

-

If your job is secure, sticking to the original repayment schedule may make more sense.

-

The best choice depends on your debt, savings, job stability, and retirement goals.

Paying off a 401(k) loan early can be a smart financial move, but it’s not always the best use of your money.

Before putting extra cash toward the balance, take a look at how it fits with your other financial priorities, your retirement savings, and your overall budget.

A clear comparison of the trade-offs can help you decide whether early repayment makes sense.

Scenarios When Early Payoff May Make Sense (and When It May Not)

Below are illustrative scenarios. Each assumes an outstanding 401(k) loan of, say, $10,000 over 5 years, with varying conditions:

| Scenario | Assumptions | If You Pay Off Early | If You Keep The Loan |

|---|---|---|---|

| High-Return Market |

Loan interest: 5% Expected return: 8% Stable job |

✓ Reinvest $10k immediately ✗ Use $10k cash today Best if: You value being debt-free more than potential investment gains. |

✓ Keep $10k cash available ✓ Repay gradually via payroll Best if: Expected investment returns exceed the loan rate. |

| High-Rate Loan (Low Market Returns) |

Loan interest: 7% Expected return: 3% Stable job |

✓ Eliminate a relatively expensive loan ✓ Save future interest payments Best if: Loan rate exceeds expected investment returns. |

✗ Continue paying a 7% loan ✓ Interest goes back into your account Best if: Cash is limited or investment outlook improves. |

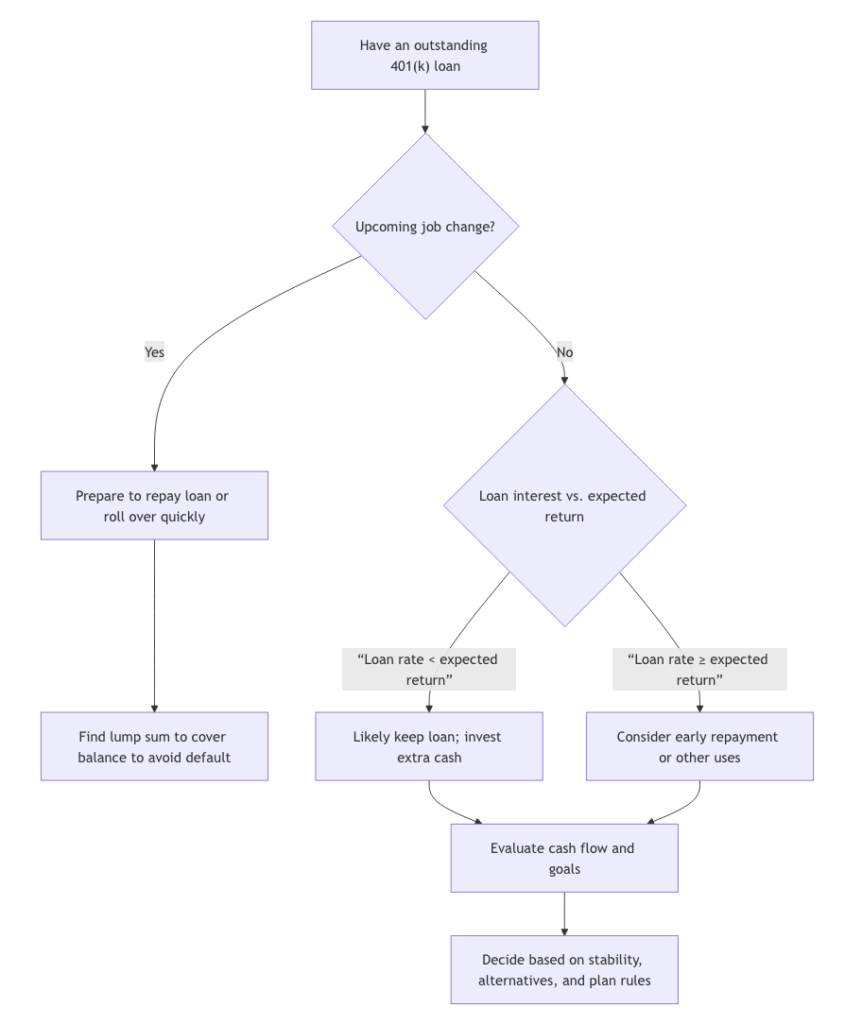

| Imminent Job Change |

Loan interest: 5% Expected return: 7% Leaving job in 6 months |

✓ Eliminate repayment risk before leaving ✓ Avoid potential taxes and penalties Best if: You expect to leave your employer soon. |

✗ May need to repay after leaving, depending on your plan ✗ Unpaid balance could become taxable and subject to penalties |

| Limited Cash, High Liquidity Needs |

Loan interest: 5% Expected return: 6% Major upcoming expenses |

✗ Tie up valuable cash ✗ May need to borrow elsewhere in an emergency Best if: You have ample emergency savings. |

✓ Preserve cash for emergencies ✓ Maintain greater financial flexibility Best if: Liquidity is a higher priority than paying off the loan. |

How Does a 401(k) Loan Work?

Unlike a personal loan or credit card, a 401(k) loan allows you to borrow money from your own retirement account.

In most cases, you can borrow up to 50% of your vested balance, up to a maximum of $50,000, and repay the loan over five years unless the funds are used for a primary residence.

While the interest you pay does go back into your retirement account, the money you borrowed is no longer invested in the market during the loan period.

That means any gains, dividends, and compounding that would have occurred on those assets are temporarily interrupted.

Benefits of Paying Off a 401(k) Loan Early

Let’s start with the reasons why paying off a 401(k) loan ahead of schedule can feel so appealing.

- Reduced default risk. If you repay now, you’ll never face the risk of a large unexpected tax bill.

- More time for contributions. You can focus on rebuilding savings or paying other debts instead of servicing the loan each paycheck.

- Peace of mind. The psychological benefit of being debt-free has no price tag.

- Prevent costly penalties. While there is no federal prepayment fee, repaying early avoids any plan rules that trigger if you partially pay.

Potential Downsides of Paying Off a 401(k) Loan Early

There are important downsides to prepaying a 401(k) loan that often tilt the balance in favor of not rushing to repay:

1. Lost investment growth

The high cost of early repayment is that you pull cash out of your investments to repay the loan.

Even if you eventually deposit it back, that money has missed potential growth.

Unless your loan interest is higher than what you realistically expect to earn in the market, keeping the loan and letting investments compound is usually better.

2. Opportunity cost of cash

To pay off early, you use after-tax cash that could be invested or used elsewhere.

Because loan repayments use after-tax dollars, you effectively double tax the interest portion:

- You paid tax on that money already and

- Will pay it again at retirement.

3. Strained liquidity

If you are using most of your liquid savings to wipe out the loan can leave you vulnerable.

Unless you have emergency savings, early payoff may leave little buffer for unexpected expenses.

So, if an emergency occurs and you’ve just drained your cash, you might need to borrow again at higher interest.

4. Reduced retirement savings growth

Money that goes to repay the loan isn’t going into new contributions.

If you divert extra cash to repay the loan, you could neglect increasing your plan contributions.

Maintaining contributions, especially any employer match, is usually crucial.

You need to keep up contributions even while repaying a loan, since pausing them can slow down your retirement savings.

5. No added tax benefit

In contrast to mortgages or student loans, 401(k) loan interest payments are not tax-deductible.

So paying down the loan doesn’t give you a tax break.

The interest simply returns to your plan, effectively canceling out.

Miss a 401(k) Loan Payment? Read This Before It’s Too Late.

A missed payment can trigger taxes, penalties, and an unexpected bill. Learn the repayment rules that every borrower should know.

Key Factors to Consider Before Paying Off

Two people with identical loan balances can reach completely different conclusions, and both can be right.

The difference usually comes down to a handful of financial factors that deserve careful consideration before you send in an extra payment.

| Key Factor | Why It Matters | What To Consider |

|---|---|---|

| Interest Rate vs. Expected Investment Return | Compare loan cost vs. investment growth | Pay early if the loan rate is higher than your expected investment return. Otherwise, keep your money invested. |

| Job Stability and Timing | Job changes can trigger repayment | If you may leave your job soon, paying off the loan early can help you avoid taxes and penalties. |

| Cash Availability | Don’t drain your savings | Keep enough cash for emergencies before paying off the loan. |

| Other Outstanding Debts | High-interest debt costs more | Pay off expensive debt, like credit cards, before a lower-rate 401(k) loan. |

| Plan Rules and Tax Implications | Every plan has different rules | Check whether your plan allows early payoff and whether any fees or restrictions apply. |

| Retirement Goals | Balance today and tomorrow | Consider whether paying off the loan or keeping your retirement savings invested better supports your long-term goals. |

Ask yourself: Is my situation one where the benefits of paying early outweigh the costs?

If not, and especially if market gains are likely to exceed the loan rate, continuing payments may be better.

I would personally prioritize emergency savings and high-interest debt before tapping more cash for a 401(k) loan payment.

Alternatives to Early 401(k) Loan Repayment

Rather than tapping your retirement funds, consider these alternatives.

| Option | Pros | Cons |

|---|---|---|

| Emergency/Savings Fund | No interest or taxes; preserves retirement accounts | Reduces your emergency cash reserve |

| 0% Balance Transfer Credit Card | May avoid interest during the promotional period | Transfer fees; high rates after the promotion; can increase debt |

| Personal Loan | Fixed payments; retirement savings remain untouched | Interest and fees; requires approval |

| Home Equity Loan or HELOC | Lower interest rates; access to larger amounts | Home serves as collateral; closing costs; foreclosure risk if you can’t repay |

| Roth IRA Contributions | Contributions can generally be withdrawn tax- and penalty-free | Limited to contributions; reduces retirement savings |

| Borrow from Family or Friends | Flexible terms; little or no interest | Can create tension or conflict if repayment becomes an issue |

You need to measure each alternative’s cost and impact.

A personal loan or HELOC keeps you out of your retirement account, but they incur interest and potential fees.

Yes, tapping savings means no interest, but it leaves you vulnerable to emergencies.

401(k) Loan Repayment FAQs

Any unpaid balance is treated as a taxable distribution, and you may owe a 10% early withdrawal penalty if you are under age 59½.

No federal penalty applies for early repayment, but check your plan rules for any administrative requirements.

You recover your principal, but you lose potential investment growth while the money is out of the market.

It depends on your plan, as some employers limit the number of loans or require a waiting period.

Interest is paid with after-tax dollars and is taxed again when withdrawn in retirement.

No. Interest paid on a 401(k) loan cannot be deducted from your taxes.

You can, but it triggers taxes and possible penalties, and permanently reduces your retirement savings.

References: